1. Introduction

To understand the looming crypto-banking crisis threatening the European Union, we first need to revisit how exposure to crypto-assets and the over-reliance on demand deposits from a single industry, played a key role in bringing down Silvergate Bank and Signature Bank in the US.

In this case study, we will,

- revisit how the two largest exchanges at the time, Binance and FTX, and their respective market makers, Cumberland and Alameda Research, operated as de facto reserve managers for a shadow dollar-based payment network for different geographies, catering to people who could not easily hold dollars or transfer them;

- re-examine the role minor stablecoins played in that shadow dollar banking system, and explore how those minor stablecoins played a key role in lubricating fiat dollar on and off-ramps; and

- analyze how the same banking problems caused by these activities in the US, now appear to be seeping into the EU through the recent proliferation of MiCA-compliant euro-backed stablecoins.

None of this analysis is intended in any way to suggest anything illegal is being perpetrated, but merely to demonstrate that many of the same practices undertaken by the crypto-asset industry in the American banking system are starting to make an appearance in the EU.

While the EU’s flagship crypto-asset legislation, the Markets in Crypto-Assets Regulation (“MiCA”) may have forced out stablecoins such as Tether’s USDT, euro-equivalent stablecoins, issued by companies backed by stablecoin issuers like Tether, may create an exploitable blind spot that facilitates continued access to fiat off-ramps through the European banking system.

2. The Shadow Dollar Banking System

We’ve previously written about how Tether’s USDT stablecoin on Ethereum and on Tron were essentially different products, serving different use cases, and different groups of customers.

At the time, the two largest exchanges and their market makers ran two parallel USDT networks on different blockchains. While FTX-Alameda Research were the primary recipients of USDT on Tron, Binance-Cumberland were the primary recipients of USDT on Ethereum.

We’ve also documented how the amounts of USDT in circulation at the time, neatly matched the dollar deposits at Signature Bank and Silvergate Bank. Given how Tether has long struggled with reliable banking facilities, it made sense that at the time these market makers were helping to fill in the gaps.

From that, we posited that FTX-Alameda Research and Binance-Cumberland, both of whom were close to Tether, had managed to carve the world up into two separate shadow dollar payment networks – one serving East Asia on Tron and the other serving the rest of the world on Ethereum.

Bahamas-based FTX-Alameda Research dominated the East Asia-focused Tron’s USDT usage, and Binance appeared to have covered everything that was outside of East Asia, including Latin America, Africa, and India.

Finally, we concluded the massive pile of dollars backing this unregulated offshore payment system was sitting in a handful of US banks, probably as demand deposits that paid no interest, providing a nice earnings boost for those banks.

Now that we’ve provided some theories as to how Tether’s USDT on different blockchains served different geographical regions, we examine how dollars were actually funneled into this shadow offshore dollar stablecoin system.

3. The Role of Minor Stablecoins

To understand the role of minor stablecoins and how they fed into the shadow offshore dollar stablecoin system dominated by Tether, we need to go back to a time when HUSD, TUSD, USDP, and GUSD (collectively, the “Minor Stablecoins”), were plying the stablecoin trade.

At the time, GUSD issued by the crypto-asset exchange Gemini, and USDP issued by Paxos Trust LLC were generally considered to have been properly backed by dollars and had in place some measure of compliance with the necessary regulations.

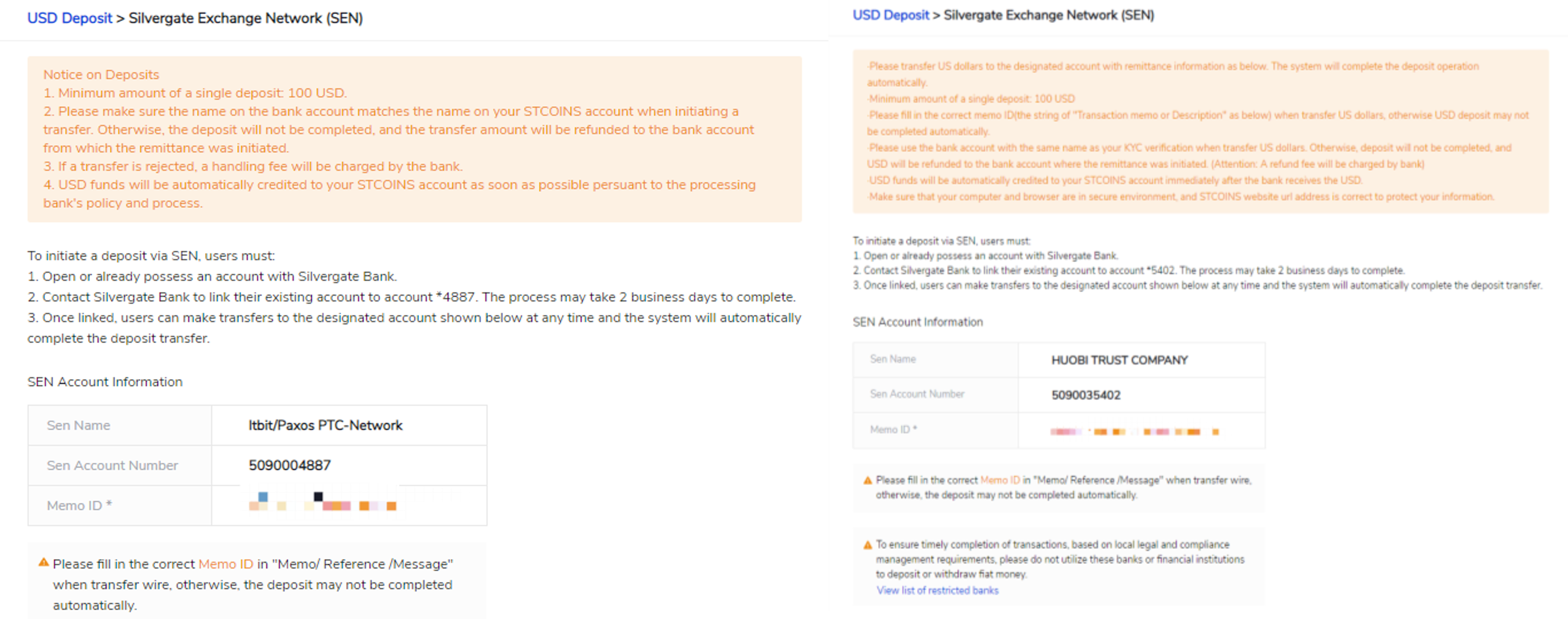

HUSD, a stablecoin product of the Huobi crypto-asset exchange (now rebranded as HTX) was run by Paxos until July 2021. When HUSD ceased being a Paxos product, the means to send dollars to HUSD shifted from Paxos to Huobi Trust Company, as seen from these archival screenshots of dollar deposits.

Notice that even though the entities receiving the dollars were different, these dollars still fed into the Silvergate Exchange Network or SEN, operated by Silvergate Bank.

Figure 1. Screenshots for Paxos Trust LLC (left) and Huobi Trust Company (right) with wire instructions for USD using the Silvergate Exchange Network operated by Silvergate Bank.

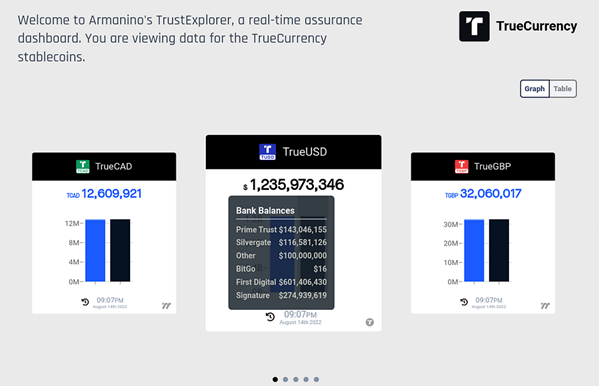

TUSD or TrueUSD provided somewhat more transparency as to where all the dollars they had were held and it used to run a website which showed which institutions held its backing assets.

Figure 2. TrueUSD attestation page with information about where TUSD's backing asssets were held. Website is no longer available.

As you can see, both Silvergate Bank and Signature Bank held significant balances for TUSD, and we also know that Prime Trust was banking at Silvergate Bank.

Now that we know where the Minor Stablecoins bank their bucks, how do we know they fed into Tether’s USDT?

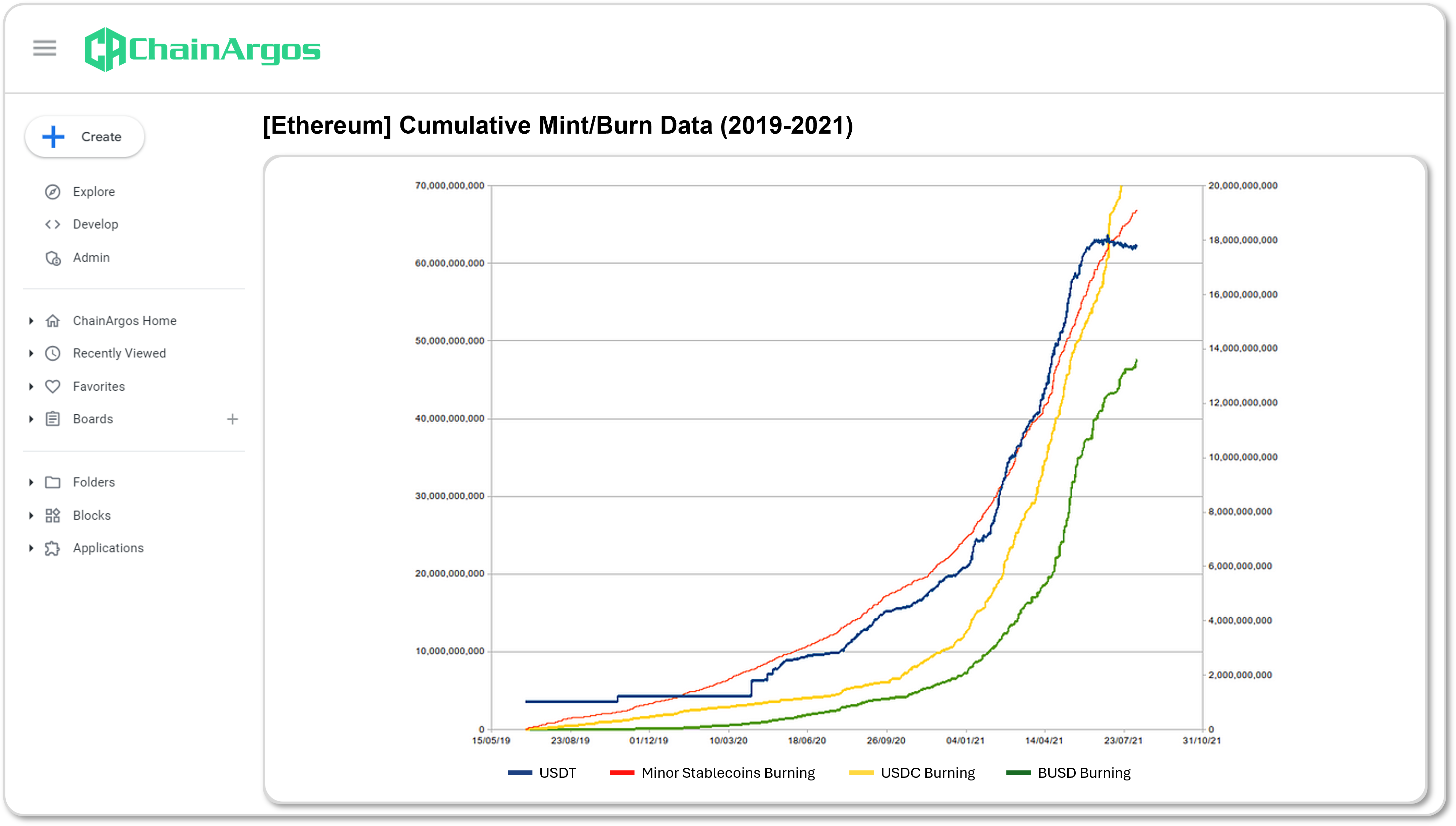

Figure 3. Cumulative USDT minting against cumulative stablecoin burning.

Between 2019 and 2021, it’s clear that the cumulative amount of Minor Stablecoins burnt and the cumulative number of USDT minted bore an uncanny correspondence, as seen from the chart above.

The pink line is for the cumulative number of Minor Stablecoins burned and the blue line is for the cumulative growth of USDT.

The yellow USDC and green BUSD cumulative burning lines don’t nearly map the USDT growth line as closely as the Minor Stablecoins.

At the time, we suggested one possibility was that the actual dollars flowing through the Minor Stablecoins ended up at Silvergate Bank and Signature Bank as possibly some kind of “outsourced” backing for USDT.

This contention was supported by the fact that far more cash appeared to be churning through the Minor Stablecoins than other stablecoins like USDC and BUSD.

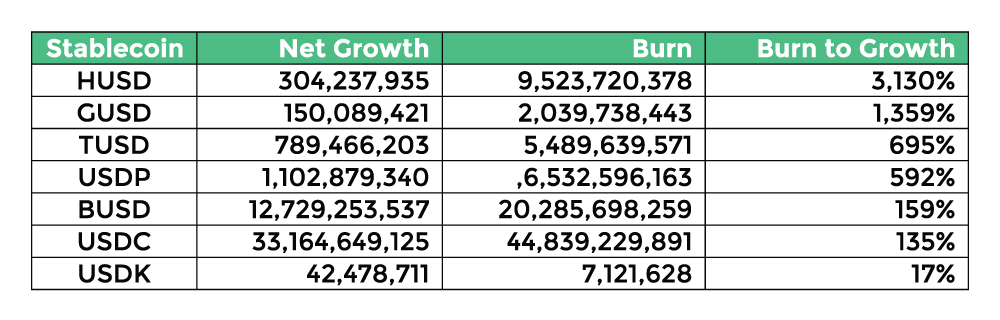

From the table above, you can clearly see that from 2018 to 2021, HUSD, GUSD, TUSD, and USDP were burned far more than the other stablecoins BUSD, USDC, and USDK.

For instance, even though HUSD had only $250 million in market cap, it had $10.5 billion in minting, and $10.25 billion in burning.

Because most of the indicators at the time (and to some extent even now) only focused on market cap and not minting and burning statistics, nobody thought very much was going on with the Minor Stablecoins at all and therefore paid little (if any) attention to them.

Take USDP for instance, the stablecoin spends much of 2020 with what appears to be an unchanged market cap, but hundreds of millions of dollars’ worth of USDP are minted and burned when its market cap was relatively stable.

Although some would cynically ascribe such transaction behavior to wash trading, that explanation doesn’t deal with the fact that the actual money has to end up somewhere.

It is of course entirely possible the funds were washed and ended up somewhere else. For example, HUSD that had been burned might have been withdrawn as cash somehow, but a far simpler explanation is that HUSD that was burned ended up in the pile which we already know about that has a similar shape and size – USDT.

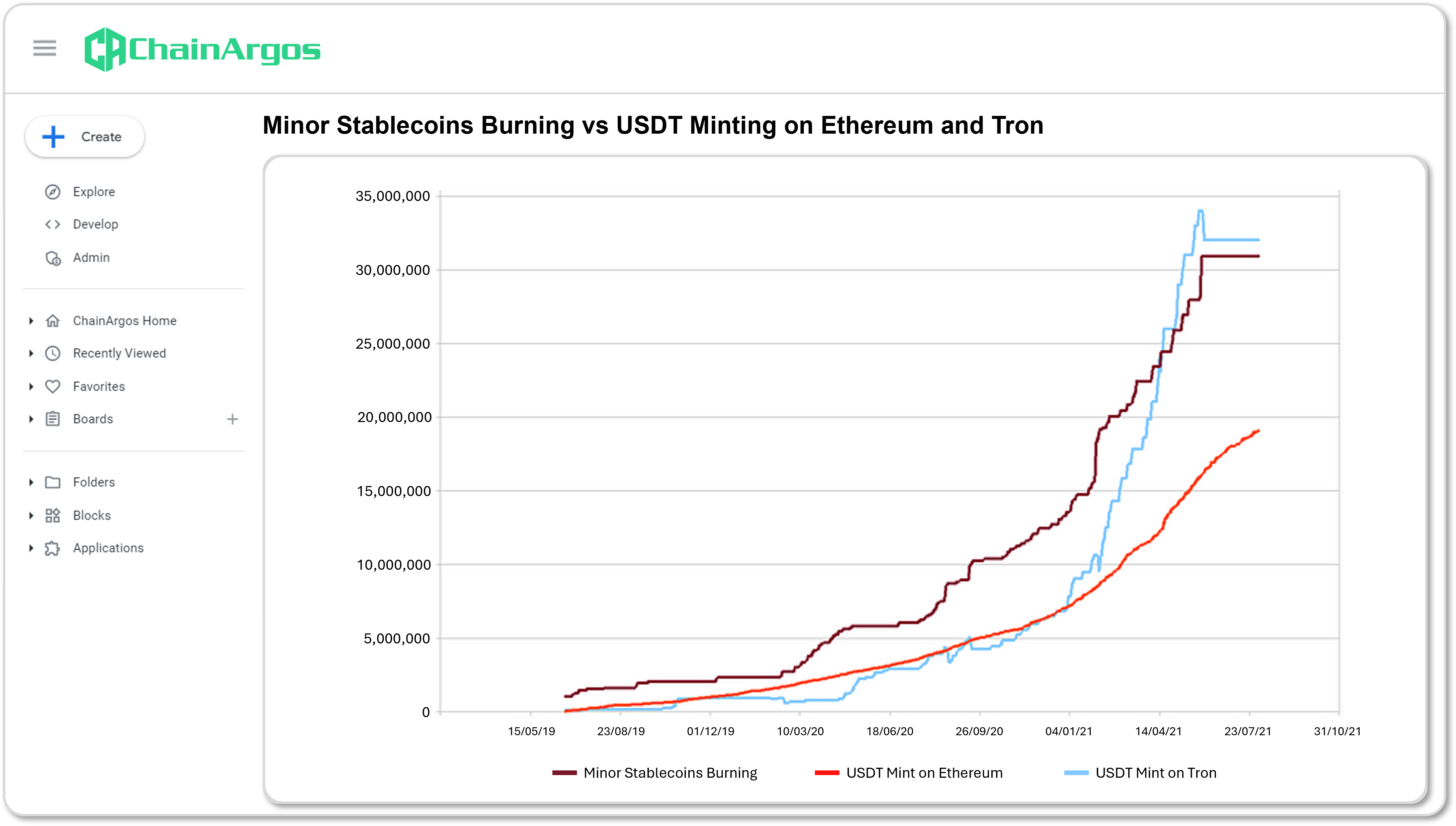

In the chart below, we see the burning of the Minor Stablecoins essentially mirroring the minting of USDT on the Ethereum and Tron blockchains between 2019 and 2020.

Figure 4. Minor Stablecoins burning (HUSD, GUSD, USDP, TUSD) vs USDT Minting on Ethereum and Tron blockchains.

Coincidentally, crypto-asset exchanges Huobi and Poloniex announced support for USDT on the Tron blockchain in March and April 2019 respectively, right after Tether commenced support for USDT on the Tron blockchain.

None of this is to say anything untoward happened during that time.

But it does appear that a sizeable amount of actual dollars traveled through the Minor Stablecoins and ended up in the larger US-based banks that served crypto-asset firms as some form of backing asset for USDT.

And it is this massive pile of dollars that would eventually create problems for the US banks that were holding them.

4. The Banks at the Center of It All

Signature Bank and Silvergate Bank were the lynchpins of the crypto-asset economy, serving as the primary dollar on and off-ramps for crypto-assets.

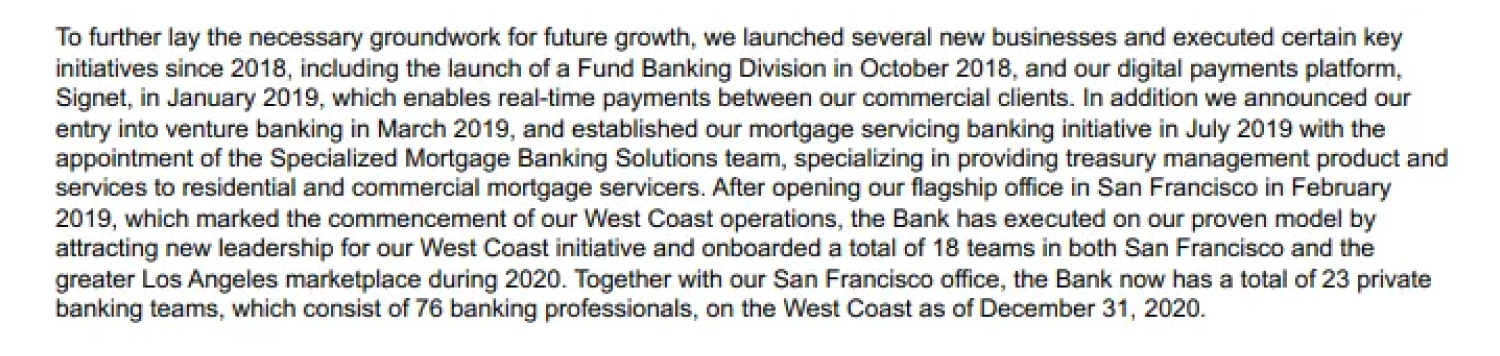

Signature Bank’s startling increase in deposits started in 2019, when they shifted their focus to target digital assets.

Figure 5. Taken from a Signature Bank’s Form 10-K. Signature Bank began focusing on digital assets in 2019. Original hyperlink may no longer be accessible.

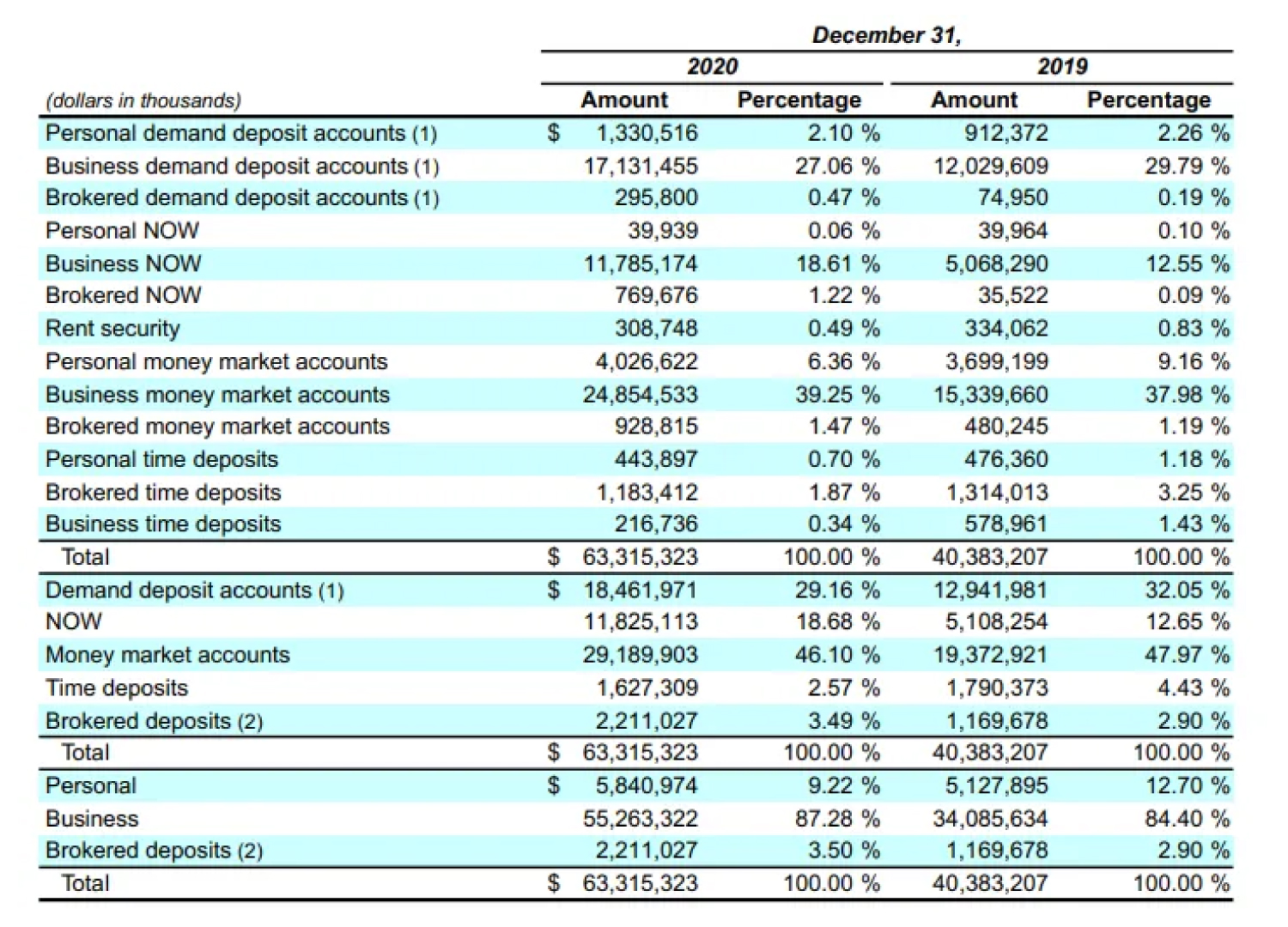

From Signature Bank’s Form 10-K filing from 2020, we see that the business demand deposit accounts saw substantial growth around the time they started to support crypto-assets.

Figure 6. from Signature Bank’s 2020 annual report. Notice how “Business demand deposit accounts” rose by almost a third between 2019 and 2020. Document may no longer be available.

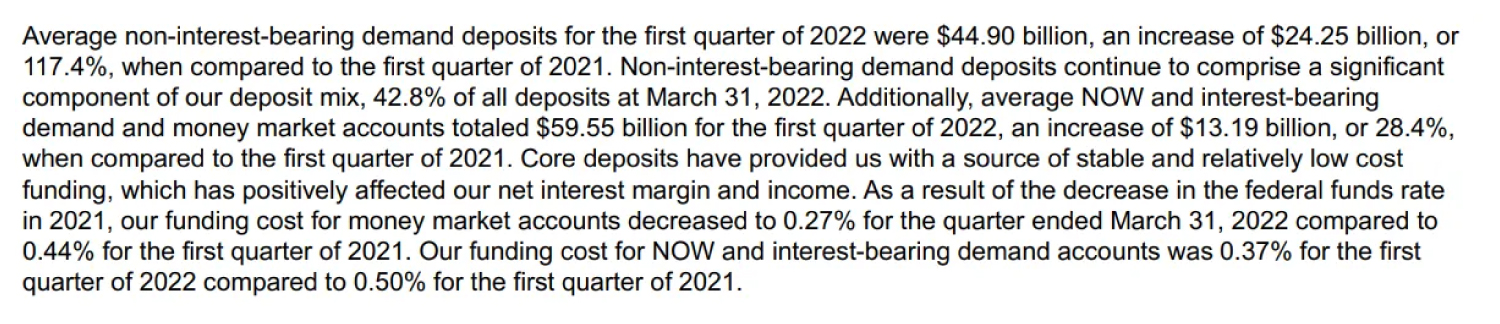

From the foregoing, it’s clear that Signature Bank was very dependent on demand deposits, and to a far higher degree than most large banks in the US. To be sure, Signature Bank themselves recognized this dependence on demand deposits, noting:

Figure 7. Extract taken from Signature Bank’s Q1 2022 Form 10-Q. Original hyperlink may no longer be accessible.

But demand deposits in and of themselves aren’t a big deal, it’s who was providing these demand deposits that mattered, and Signature Bank made clear it was their digital asset customers who formed the bulk of their demand deposits.

Figure 8. Extract taken from Signature Bank’s Q2 2021 Form 10-Q. Original hyperlink may no longer be accessible.

Silvergate Bank was also similarly active in the crypto-asset space as evidenced by their Q3 2019 Form 10-Q filing:

Figure 9. Extract taken from Silvergate Bank’s Q3 2019 Form 10-Q. Original hyperlink may no longer be accessible.

Figure 10. Extract taken from Silvergate Bank's Q3 2019 Form 10-Q, describing the bank's Silvergate Exchange Network or SEN. Original hyperlink may no longer be accessible.

And who were Silvergate Bank’s customers? The same customers served by Signature Bank – the digital asset industry.

Figure 10. Extract taken from Silvergate Bank's Q3 2019 Form 10-Q, describing the bank's Silvergate Exchange Network or SEN. Original hyperlink may no longer be accessible.

Silvergate Bank also disclosed their deposit base, and it’s obvious that they never had any meaningful interest-bearing accounts, it was almost entirely non-interest bearing demand deposits.

Figure 11. Extract taken from Silvergate Bank’s Q3 2020 Form 10-Q.

Now that we’ve established that Signature Bank and Silvergate Bank were the primary bankers to the crypto-asset industry, let’s see if we can find any correlations.

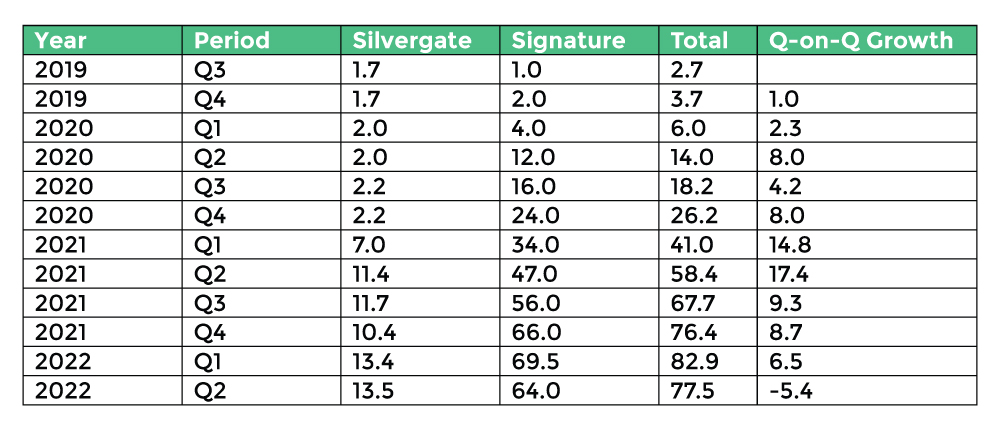

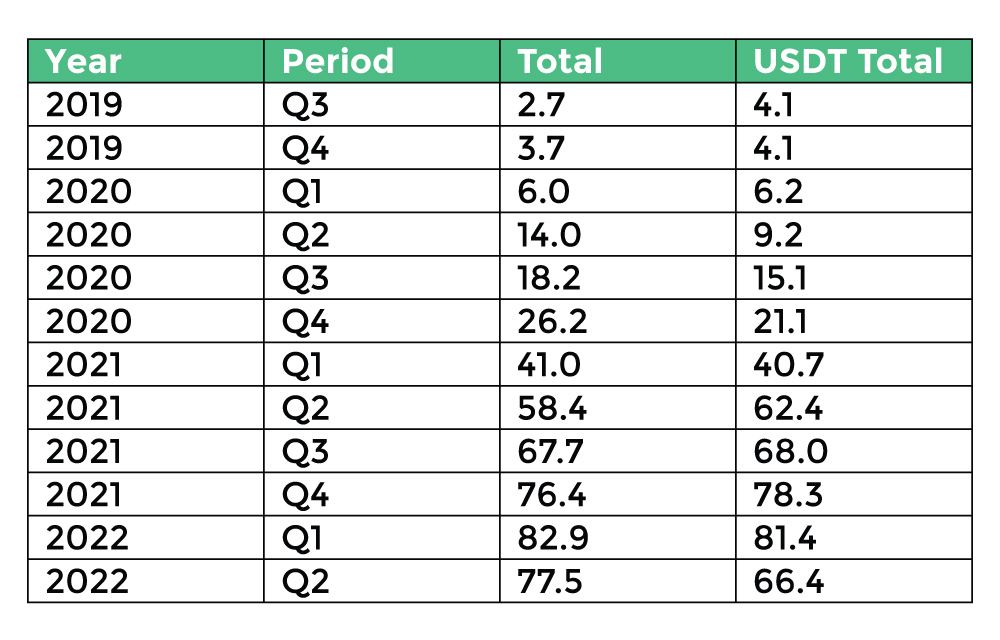

While Silvergate Bank was a tiny bank before their pivot to crypto-assets, Signature Bank was much larger.

Subtracting the $30 billion that Signature Bank started with and adding Signature Bank’s demand deposit increases together with Silvergate Bank’s we can create the following table.

The totals are shockingly similar to another closely-watched total at the time – the amount of Tether outstanding:

There is absolutely no reason these numbers should match up so neatly, especially given Tether was not officially holding their cash reserves at these banks. In fact, this was around the time that Tether declared it was primarily holding commercial paper.

But it does allow for a theory to be posited, that while Tether may not have been banking directly with Silvergate Bank and Signature Bank (for obvious reasons), it is possible Tether’s commercial paper consisted of obligations of whoever held these demand deposits at the banks.

While it is a terrible abuse of language to equate promising someone else your bank deposit to commercial paper, it is analogous to a kind of certificate of deposit, or even an accounts receivable instrument.

In any event, we know that prior to the collapse of Silvergate Bank and Signature Bank, they were heavily reliant on demand deposits from crypto-asset customers, and therein lay the problem.

Demand deposits are funds that customers can withdraw at any time and this makes them inherently volatile, especially when they come from a sector as prone to swings as the crypto-asset markets.

In 2022, the collapse of Terra-LUNA, FTX, 3AC, Celsius, and Voyager, and the rapid decline in crypto-asset values, saw customers withdraw funds from Signature and Silvergate en masse, creating a liquidity crisis for these banks.

The sudden and large-scale withdrawals forced Silvergate and Signature Bank to sell off assets, often at a loss, to meet their obligations, further eroding their financial stability, creating a loss of confidence among the remaining non-crypto depositors, fueling a run on the banks.

5. Could a US-Style Crisis hit the EU?

We previously prepared a detailed case study on the MiCA-compliant EURI stablecoin issued by the Luxembourg-based Banking Circle S.A. and noted how the only counterparty to have redeemed EURI for euros in the banking system, appeared linked to the crypto-asset exchange Binance and First Digital Trust Limited.

It appears that EURI is possibly being used as a euro off-ramp for FDUSD and other stablecoins, and such a use case would be consistent with what was seen in the American experience, where Minor Stablecoins were feeding into Tether’s USDT.

Now StablR, a recently launched service provider backed by Tether, and which holds a Maltese Electronic Money Institution (EMI) license, has launched EURR, a new euro-backed stablecoin.

The largest receiver of EURR is an address linked to Cumberland (“0x091d Address”).

Figure 12. Largest Receivers of the EURR token over the preceding 90 days. Notice that an address linked to Cumberland (either a customer or Cumberland themselves), Bitfinex (associated with Tether) and Kraken are the largest recipients of EURR.

The 0x091d Address processes a significant volume of stablecoins, facilitating deposits of billions of dollars worth of USDC, USDT, FDUSD, and other tokens to a wide range of exchanges.

Figure 13. Largest Counterparties for the 0x091d Address associated with Cumberland and transacting billions of dollars worth of stablecoins primarily with Binance and Cumberland.

The 0x091d Address’ largest deposits are to Binance and it is also one of the largest transactors of FDUSD, depositing almost $200 million worth of FDUSD to a Binance deposit address.

Figure 14. Largest Counterparties for the 0x091d Address associated with Cumberland, filtered for FDUSD only, and displaying how almost $200 million worth of FDUSD was sent by this address to Binance.

FDUSD is a stablecoin used almost exclusively on Binance and issued by a Hong Kong trust company associated with a stablecoin-related fraud settlement with the US Securities and Exchange Commission.

But the largest senders and receivers of FDUSD are also either Binance or Cumberland.

Figure 15. Largest Senders of FDUSD. Besides First Digital Labs, which is associated with the issuance of FDUSD, the main sender of FDUSD is Binance, and the market maker Wintermute.

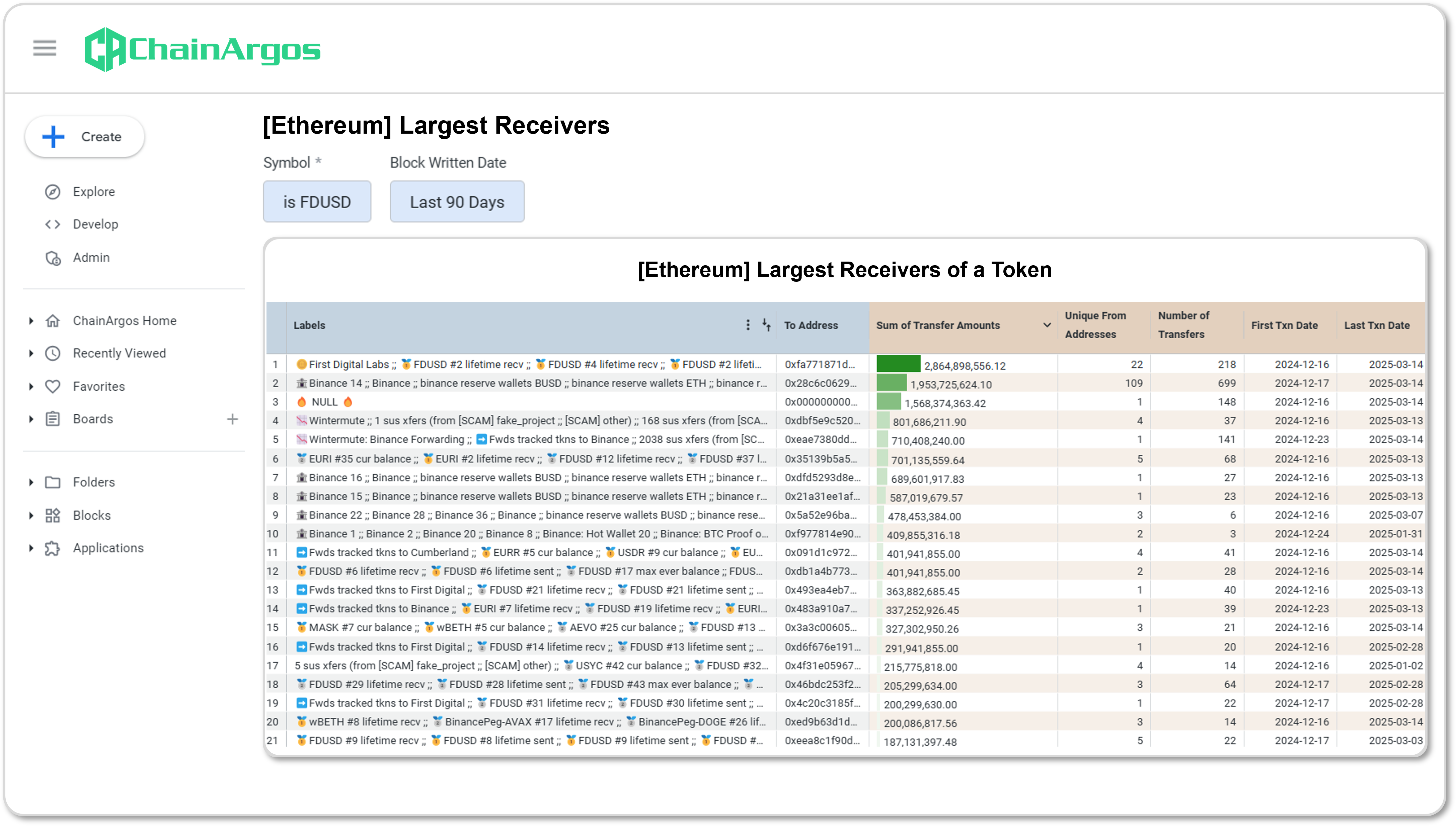

Figure 16. Largest Receivers of FDUSD. Besides First Digital Labs, which is associated with the issuance of FDUSD, the main receiver of FDUSD is Binance, and the market maker Wintermute.

That Binance is one of the major counterparties for EURR since its launch, using some of the same addresses used previously to transact FDUSD, suggests the exchange is setting up to do the same thing in Europe that it had done previously in the US.

There is insufficient volume in EURR at this point (fewer than 20 addresses have received more than one thousand EURR as of this writing and none has received more than 10 million) to establish what EURR is being used for.

But we can already see EURR reusing infrastructure and frameworks linked to many recent problems that for the most part had stopped following a wide range of legal and enforcement actions.

It’s worth noting that exchanges operating in the EU, including Binance, are delisting Tether’s USDT, but recall that EURR has a MiCA license and Tether backs EURR’s issuer.

That the same cluster of counterparties is reusing the same frameworks and infrastructure they had in place previously, only in euros this time instead of dollars, and in the European banking system this time instead of the American one, strongly suggests an intention to engage in the same sort of conduct seen previously.

Again, none of this is to suggest that anything illegal or nefarious is happening, but rather to highlight that some of the very same risks that were crystalized in the US banking system are starting to appear in the EU banking system.

Insofar as regulators are aware of such risks and exercising adequate oversight of the relevant financial institutions within their regulatory ambit, then there isn’t a whole lot to be concerned about.